|

|

|

机器学习中有哪些涉及统计因果推断的算法?

机器学习分析数据似乎强调利用数据之间的相关关系进行预测,想知道是否有些算法设计因果推断的理论?

关注者

82

被浏览

50,933

7 个回答

这里介绍下微软开发的 DoWhy框架和因果森林(EconML包),其核心算法是 Double Machine Learning。以下提供了一个官方案例进行具体说明。

DoWhy 的作用:

- 建立因果模型(LinearDML)(DML: LinearDL, CausalForestDML)

- 识别影响效果(LinearDML.dowhy.fit(): Backdoor,Frontdoor,IV)

- 检验因果假设 - 稳健性检验(添加随机共同原因变量、安慰剂检验、随机删除部分样本)

EconML DML 估计器的作用:

- 考虑干预的变动

- 分析影响的异质性

- EconML CATE SingleTreeCateInterpreter -- 展示各个 features 的作用大

- EconML CATE SingleTreePolicyInterpreter -- 提出最优政策方案,即指出具体的细分样本+干预方案,以达到收益最大

本例中的最优政策方案:指出具体的细分顾客群体,对应的折扣方案,及对应的总收益(考虑折扣带来的成本)

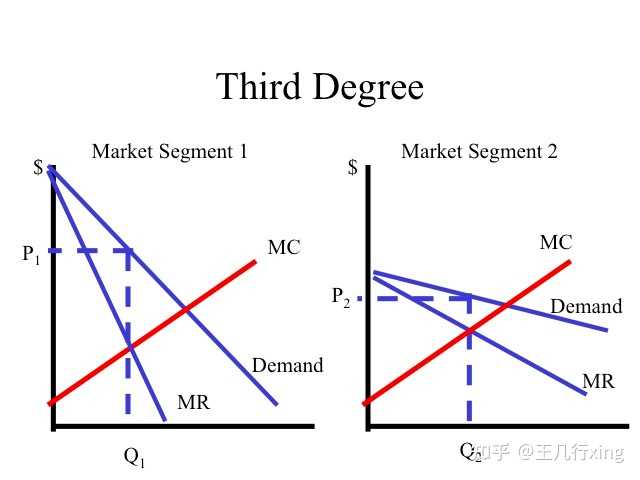

案例说明: 找出最优的促销方案,决定给不同收入水平的顾客,提供不同的折扣方案,以达到利润最大化。

btw,三级价格歧视的极端情况下,是为每一个消费者制定一个ta最高能接受的价格,以实现利润最大化。

1. 数据准备

## 准备工作

import warnings

warnings.simplefilter('ignore')

import os

import urllib.request

import numpy as np

import pandas as pd

from networkx.drawing.nx_pydot import to_pydot

from IPython.display import Image, display

## 导入机器学习包的相关工具

from sklearn.preprocessing import PolynomialFeatures

from sklearn.ensemble import GradientBoostingRegressor

## 导入 EconML 包的相关工具

from econml.dml import LinearDML, CausalForestDML

from econml.cate_interpreter import SingleTreeCateInterpreter, SingleTreePolicyInterpreter

import matplotlib.pyplot as plt

%matplotlib inline

%config InlineBackend.figure_format = 'retina'

## 数据导入

file_url = "https://msalicedatapublic.blob.core.windows.net/datasets/Pricing/pricing_sample.csv"

train_data = pd.read_csv(file_url)

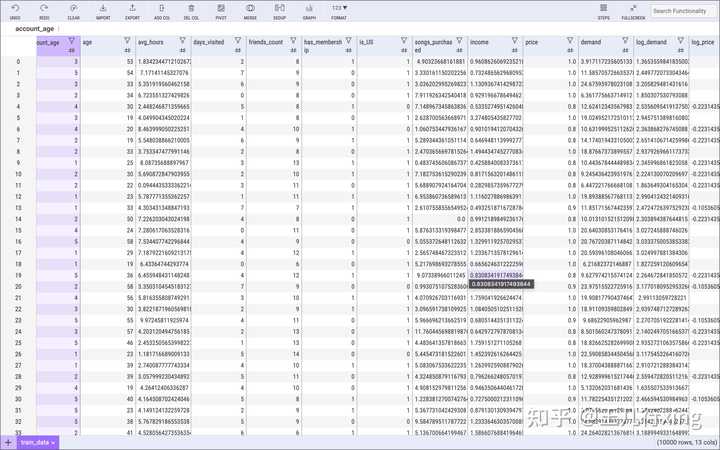

train_data.head()

train_data.describe()

查看数据:

## 变量转换

## 结果变量 target

train_data["log_demand"] = np.log(train_data

["demand"])

train_data["log_price"] = np.log(train_data["price"])

Y = train_data["log_demand"].values ## from Series to np array

## 干预变量 treatment

T = train_data["log_price"].values

## 关键自变量

X = train_data[["income"]].values

## 混淆变量 - 控制变量

confounder_names = ["account_age", "age", "avg_hours", "days_visited", "friends_count", "has_membership", "is_US", "songs_purchased"]

W = train_data[confounder_names].values

## 构造关键自变量的测试数据

X_test = np.linspace(0, 5, 100).reshape(-1, 1)

X_test_data = pd.DataFrame(X_test, columns=["income"])2. DoWhy: 构建因果框架

## 初始化 EconML 估计器

est = LinearDML(model_y=GradientBoostingRegressor(), model_t=GradientBoostingRegressor(),

featurizer=PolynomialFeatures(degree=2, include_bias=False))

## 通过 DoWhy 进行拟合

est_dw = est.dowhy.fit(Y, T, X=X, W=W, outcome_names=["log_demand"], treatment_names=["log_price"], feature_names=["income"],

confounder_names=confounder_names, inference="statsmodels")

## 画出因果图

try:

# Try pretty printing the graph. Requires pydot and pygraphviz

display(

Image(to_pydot(est_dw._graph._graph).create_png())

except:

# Fall back on default graph view

est_dw.view_model()

## 输出估计结果

identified_estimand = est_dw.identified_estimand_

print(identified_estimand)

[Out: ]

Estimand type: nonparametric-ate

### Estimand : 1

Estimand name: backdoor

Estimand expression:

────────────(Expectation(log_demand|friends_count,income,avg_hours,account_age

d[log_price]

,is_US,days_visited,age,has_membership,songs_purchased))

Estimand assumption 1, Unconfoundedness: If U→{log_price} and U→log_demand then P(log_demand|log_price,friends_count,income,avg_hours,account_age,is_US,days_visited,age,has_membership,songs_purchased,U) = P(log_demand|log_price,friends_count,income,avg_hours,account_age,is_US,days_visited,age,has_membership,songs_purchased)

### Estimand : 2

Estimand name: iv

No such variable found!

### Estimand : 3

Estimand name: frontdoor

No such variable found!3. EconML: 估计因果效应

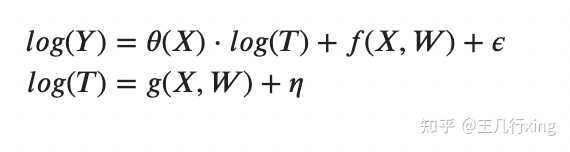

具体的估计模型如下(和计量中的中介效应在形式上有点相似)

## 基于真实的数据生成过程,估计因果效应

def gamma_fn(X):

return -3 - 14 * (X["income"] < 1)

def beta_fn(X):

return 20 + 0.5 * (X["avg_hours"]) + 5 * (X["days_visited"] > 4)

def demand_fn(data, T):

Y = gamma_fn(data) * T + beta_fn(data)

return Y

def true_te(x, n, stats):

if x < 1:

subdata = train_data[train_data["income"] < 1].sample(n=n, replace=True)

else:

subdata = train_data[train_data["income"] >= 1].sample(n=n, replace=True)

te_array = subdata["price"] * gamma_fn(subdata) / (subdata["demand"])

if stats == "mean":

return np.mean(te_array)

elif stats == "median":

return np.median(te_array)

elif isinstance(stats, int):

return np.percentile(te_array, stats)

## 估计结果和置信区间

truth_te_estimate = np.apply_along_axis(true_te, 1, X_test, 1000, "mean")

truth_te_upper = np.apply_along_axis(

true_te, 1, X_test, 1000, 95)

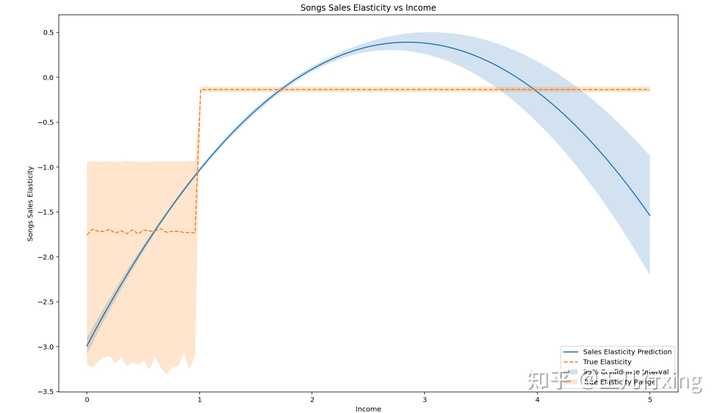

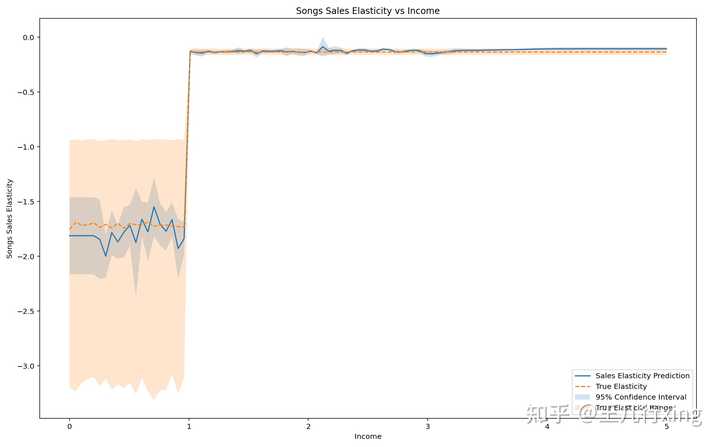

truth_te_lower = np.apply_along_axis(true_te, 1, X_test, 1000, 5) 接下来,对估计的结果和真实情况进行对比:

plt.figure(figsize=(16, 10))

plt.plot(X_test.flatten(), te_pred, label="Sales Elasticity Prediction")

plt.plot(X_test.flatten(), truth_te_estimate, "--", label="True Elasticity")

plt.fill_between(

X_test.flatten(),

te_pred_interval[0].flatten(),

te_pred_interval[1].flatten(),

alpha=0.2,

label="95% Confidence Interval",

plt.fill_between(

X_test.flatten(),

truth_te_lower,

truth_te_upper,

alpha=0.2,

label="True Elasticity Range",

plt.xlabel("Income")

plt.ylabel("Songs Sales Elasticity")

plt.title("Songs Sales Elasticity vs Income")

plt.legend(loc="lower right")

上图解读:

- 真实的干预效果非线性(橘色虚线)

- 拟合的模型基于 income 的二次项(且二次项的系数为负,抛物线开口向下)

- 不管是真实还是拟合的结果都能看出,收入低弹性高,收入高弹性低(这好像是个常识?)

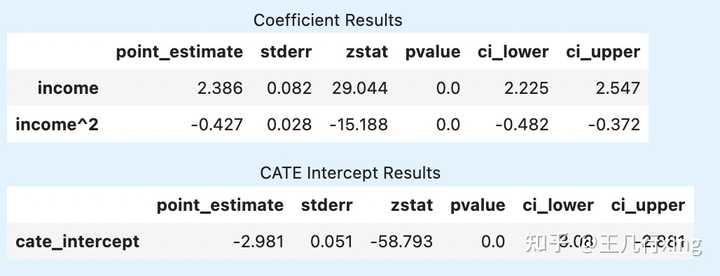

查看具体的估计结果系数:

## 显示X和截距项的估计结果信息

est_dw.summary(feature_names=["income"])

非参估计与HTE: CausalForestDML

前面的估计我们使用了线性的模型,发现估计效果整体虽然还行,但是离真实情况仍有显著差距。这里我们转向非参估计,基于因果森林重新对数据进行建模和拟合。

## 初始化

est_nonparam = CausalForestDML(model_y=GradientBoostingRegressor(), model_t=GradientBoostingRegressor())

## 通过 DoWhy 进行拟合

est_nonparam_dw = est_nonparam.dowhy.fit(Y, T, X=X, W=W, outcome_names=["log_demand"], treatment_names=["log_price"],

feature_names=["income"], confounder_names=confounder_names, inference="blb")

## 计算干预效应及其置信区间

te_pred = est_nonparam_dw.effect(X_test).flatten()

te_pred_interval = est_nonparam_dw.effect_interval(X_test)

## 比较非参估计的结果和真实结果

plt.figure(figsize=(16, 10))

plt.plot(X_test.flatten(), te_pred, label="Sales Elasticity Prediction")

plt.plot(X_test.flatten(), truth_te_estimate, "--", label="True Elasticity")

plt.fill_between(

X_test.flatten(),

te_pred_interval[0].flatten(),

te_pred_interval[1].flatten(),

alpha=0.2,

label="95% Confidence Interval",

plt.fill_between(

X_test.flatten(),

truth_te_lower,

truth_te_upper,

alpha=0.2,

label="True Elasticity Range",

plt.xlabel("Income")

plt.ylabel("Songs Sales Elasticity")

plt.title("Songs Sales Elasticity vs Income")

plt.legend(loc="lower right")

上图解读:

- 拟合效果远好过线性模型(LinearDML)

- 估计结果置信区间完全覆盖真实情况

- 同样的,估计结果显示收入低弹性高,收入高弹性低

4. DoWhy:稳健性检验

4.1 加入一个随机的共同原因变量

res_random = est_nonparam_dw.refute_estimate(method_name="random_common_cause")

print(res_random)

[Out: ]

Refute: Add a Random Common Cause

Estimated effect:-0.9561140448923923

New effect:-0.963688374616349结果解读:点估计结果变化不大。

4.2 加入一个无法观测到的的共同原因变量

res_unobserved = est_nonparam_dw.refute_estimate(

method_name="add_unobserved_common_cause",

confounders_effect_on_treatment="linear",

confounders_effect_on_outcome="linear",

effect_strength_on_treatment=0.1,

effect_strength_on_outcome=0.1,

print(res_unobserved)

[Out: ]

Refute: Add an Unobserved Common Cause

Estimated effect:-0.9561140448923923

New effect:0.1932125423770007结果解读:点估计结果变化较大,但是仍然不等于0?(这里为什么不显示p值?)。

4.3 安慰剂检验

这里所谓安慰剂检验,就是把干预变量(价格)替换成一个噪音变量,理想的结果是估计的系数接近于,或者p值不显著。

res_placebo = est_nonparam_dw.refute_estimate(

method_name="placebo_treatment_refuter", placebo_type="permute",

num_simulations=3

print(res_placebo)

[Out: ]

Refute: Use a Placebo Treatment

Estimated effect:-0.9561140448923923

New effect:-0.00769355893605958

p value:0.21924855198612314解读:点估计的结果变化较大,且p值不在显著。(难道是如果显著就不显示p值?)

4.5 随机删除部分数据

res_subset = est_nonparam_dw.refute_estimate(

method_name="data_subset_refuter", subset_fraction=0.8,

num_simulations=3)

print(res_subset)

Refute: Use a subset of data

Estimated effect:-0.9561140448923923

New effect:-0.957908388178223

p value:0.022684332959365117估计结果相差不大,并且显著(显示了p值!)

5. EconML:干预的异质性

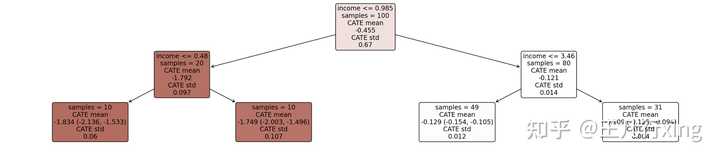

intrp = SingleTreeCateInterpreter(include_model_uncertainty=True, max_depth=2, min_samples_leaf=10)

intrp.interpret(est_nonparam_dw, X_test)

plt.figure(figsize=(25, 5))

intrp.plot(feature_names=["income"], fontsize=12)

结果解读:左边深色区域表示价格弹性较大,右边结果显示较小,即对打折的反应是不同的。

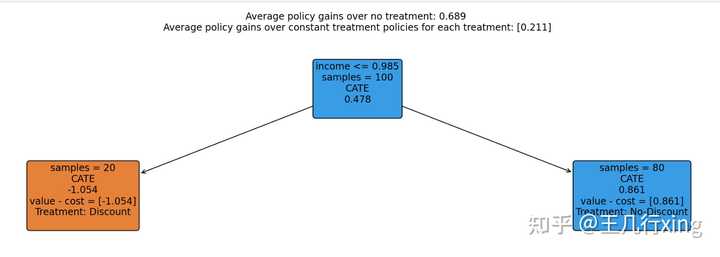

5.1 SingleTreePolicyInterpreter: CATE 模型的解释

intrp = SingleTreePolicyInterpreter(risk_level=0.05, max_depth=2, min_samples_leaf=1, min_impurity_decrease=0.001)

intrp.interpret(est_nonparam_dw, X_test, sample_treatment_costs=-1)

plt.figure(figsize=(25, 5))

intrp.plot(feature_names=["income"], treatment_names=["Discount", "No-Discount"], fontsize=12)

5.2 比较不同的打折策略

## 定义折扣策略收益函数

def revenue_fn(data, discount_level1, discount_level2, baseline_T, policy):

policy_price = baseline_T * (1 - discount_level1) * policy + baseline_T * (1 - discount_level2) * (1 - policy)

demand = demand_fn(data, policy_price)

rev = demand * policy_price

return rev

policy_dic = {}

## 本文的策略

policy = intrp.treat(X)

policy_dic["Our Policy"] = np.mean(revenue_fn(train_data, 0, 0.1, 1, policy))

## 原始策略

policy_dic["Previous Strategy"] = np.mean(train_data["price"] * train_data["demand"])

## 对所有人都打折

policy_dic["Give Everyone Discount"] = np.mean(revenue_fn(train_data, 0.1, 0, 1, np.ones(len(X))))

## 对所有人都不打折

policy_dic["Give No One Discount"] = np.mean(revenue_fn(train_data, 0, 0.1, 1, np.ones(len(X))))

## 对穷人打折,对富人涨价